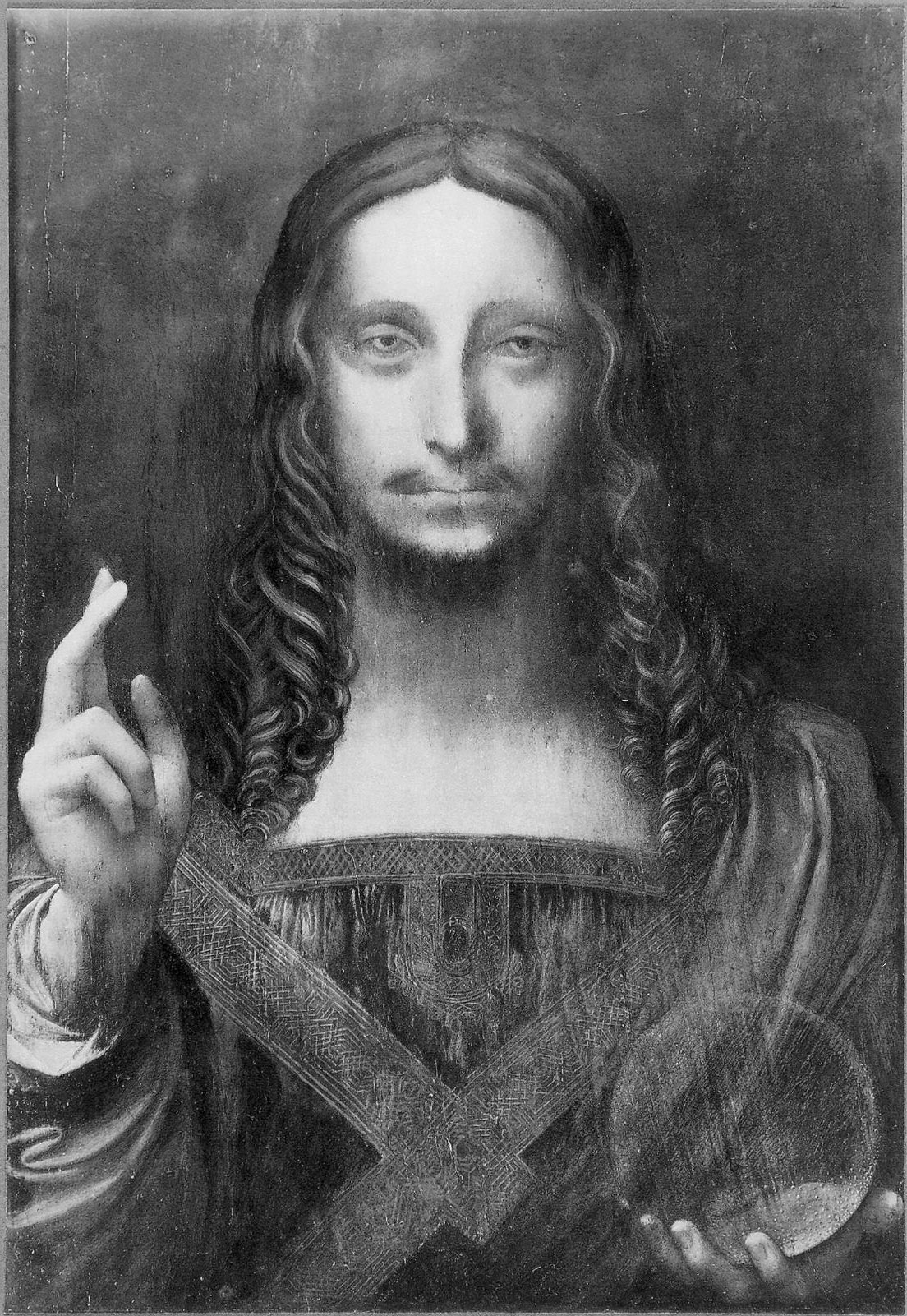

Before we left for Paris, Christie’s sold Leonardo’s “Salvator Mundi” for USD $450,312,500 (buyer’s premium included). Almost half a billion dollars spent in one night, and all for a single painting. And one whose provenance and attribution were both … interesting… (The painting has an convoluted history, and as Christie’s condition report notes, was quite damaged when it was “discovered” at an auction in 2005. It was restored in 2007 by Dianne Dwyer Modestini (Institute of Fine Arts, NYU). It looked like this before the restoration. In a 2012 review of the Leonardo survey at the National Gallery (London), Carmen Bambach wrote, “Much of the original painting surface may be by [Leonardo’s student Giovanni Antonio] Boltraffio,” while Frank Zoellner argued that it was “a high quality product of Leonardo’s workshop.” Both Bambach and Zoellner agree that Leonardo was personally involved with the production of the painting, but did not do most (or all) of the painting. Leonardo scholar Martin Kemp stands by the autograph attribution to Leonardo. In any case, the sale led to this Instagram post from Tom Campbell, the ex-director of the Metropolitan Museum of Art, which was itself the subject of some fascination.)

After the sale, so many questions: Who was the buyer? Who in their right mind would spend almost half a billion dollars on a single work of art? Why do really rich people buy art anyway? (A recent UBS Investor Watch report says the rich buy for “passion,” not profit–the report’s alternate title is “for love, not money.” According to the report, “collectors willingly let emotions dictate their decisions,” and “wealthier collectors are more passionate about art.” And 22% of these “wealthier investors (those with $5 million or more in investable assets)” apparently “spend more on [their] collection than they save for retirement.” What I want to know: who are these people?) And what does that say about the art market, our culture, the widening global inequality between “High Net Worth Individuals” and … everyone else?

Last week, new reports kept surfacing: first, the buyer was an obscure Saudi prince named Prince Bader bin Abdullah bin Mohammed bin Farhan al-Saud, then, the buyer was actually the Saudi Crown Prince Mohammed Bin Salman. It seems that all of these princes were acting as proxies for Abu Dhabi’s Department of Culture and Tourism. One thing is certain: the Salvator Mundi is headed for the Louvre Abu Dhabi, as the museum announced on Twitter. (The initial announcement didn’t reveal that the museum had actually bought the painting.)

Now that I’m back in New York, and counting down the hours until a vote on the new Republican tax bill, the Salvator Mundi sale keeps creeping back into my mind, as an emblem of the way that these blockbuster art prices serve as bellwethers of inequality. Take a look at this chart. And then take a look at this 2016 study by Thomas Piketty, Emmanuel Saez, and Gabriel Zucman. Let’s leave it at that.

a postscript on the art market, c. 2017

Clare McAndrew noted in her Art Market 2017 report, “The high end has been growing the fastest over the past ten years.” From the same report: “This changing structure of the art market by value has come alongside very little change in the share of the volume of sales. The low end accounted for the majority of transactions in 2016 (94%) and this has fluctuated in a fairly narrow band over ten years (between 89% and 94%). The high end, on the other hand, has never exceeded 1% of the volume of transactions. Because of the dominance of sales at the high end of the market in the key art market hubs, geographical market share also fluctuates considerably with price level. The top three markets of the US, China and the UK still made up the majority of sales in all price segments in 2016, but their share increases with increasing prices, particularly in the case of the US, where most of the biggest auctions currently take place. […] “The top-heavy nature of the market in recent years also extends to the artists whose works sell a auction, with much of the value centered on a very narrow segment of artists. In 2016 there were around 48,380 unique artists whose work sold at fine art auctions around the world. Close to half of the value of sales in 2016 (48%) came from just 1% of those artists.” (119-120)

The report also notes that the middle market for art and antiques is disappearing. This is not unique to the art market. Changes to global wealth structures means that the middle market for just about everything is disappearing. The art market reflects the bipolar structure of contemporary global wealth — there’s growth at both the low and high ends, and a shrinking middle.

{kind=link}

Leave a comment